Rambling about the Maths of Debt

The other day, Kevin Williamson posted this about balancing the Federal Budget. It is the typical snarling, snide polemic he is known for recently. Maybe he accidentally drank out of his ink bottle or took a blow to the head, but his work has been of this type for a while. This recent piece is mostly another deranged rant about Donald Trump. The bulk of his column is crap, but this got my attention.

At the moment, our national fiscal situation is considerably less bad than it was during the Obama-Pelosi-Reid era of one-party Democratic rule; the 2010 and 2011 federal deficits were 8.7 and 8.5 percent of GDP, respectively, but the 2014 deficit was only 2.8 percent of GDP. Federal spending went from 24.4 percent of GDP in 2009 to 20.3 percent in 2014, thanks in no small part to budget sequestration, the one national policy in which Washington’s Democrats and Washington’s Republicans are united in loathing. The 2017 deficit is projected to be 2.3 percent of GDP.

That puts us within striking distance of having a balanced budget (albeit one that is balanced at a spending point that is too high for my own taste) or at least the reduction of budget deficits to trivial levels. All that is needed to get there is a little sober reform on the taxing front and a little sober reform on the spending front, with the hardest piece being reform of our entitlement programs, which in the long run will be the major drivers of deficits. I like the idea of radical tax reform, scrapping the tax code, abolishing the IRS, and starting over, and then privatizing Social Security and abolishing Medicare and Medicaid to boot. But you don’t actually have to do that to balance the budget.

That struck me as implausible so I did some mathing. The first thing we need to know is how much debt the Feds are piling on each year. In fact, that’s probably the only thing worth knowing as that is the tax on the future we may or may not be able to sustain. Greece stopped being a country, after all, because it could not service its debt, not because it spent too much or taxed too little. When you can no longer service your debt, you’re done as a country.

According to the Treasury, the amount of total debt held by the public has gone up 23.9% since the heroic budget deal Williamson is fond of touting. That’s better than the previous four years when debt rose by 37%, but there was also the big giant recession where tax receipts dropped. On the other hand, it is still well above the average over the last 35 years, so no one should be celebrating this modest reduction.

The larger point he is making is that with some small tweaks, the federal budget can be balanced. Well, over the last 35 years the annual increase in Federal debt has been 8.3%. In 1980 the debt was $907,701,000,000 and it is now $17,824,071,380,733, as of the end of the 2014 fiscal year. That’s a staggering amount of debt that happened during the two biggest economic booms in the nation’s history. Put another way, in the best of times we have run up debt at record levels.

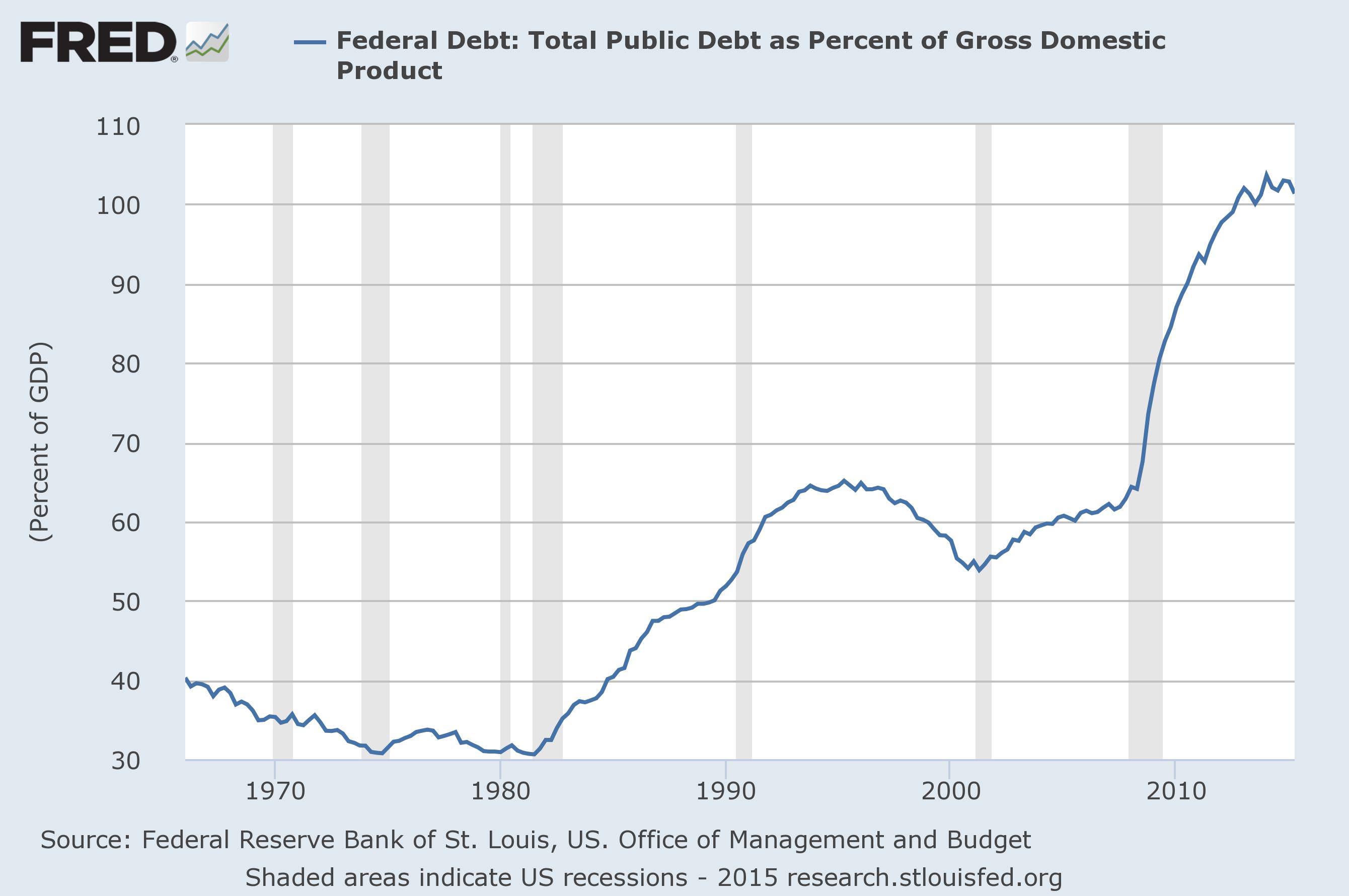

For another way to look at it, here is the inflation adjusted debt since the 60’s:

{kind=link}

There’s no way a sober person can look at the number and come away thinking we are a few tweaks away from solving the debt problem. If that were true, the graph above would not exist. Instead the line would bounce along in that 30% range as it had for so long. Something changed in the 1980’s and as a result debt as been on a steady run upward ever since, regardless of the party in charge and the amount of tweaking.

That raises another interesting question. If debt as a percentage of GDP is spiraling upward and neither party seems to have a way to stop it, what is driving the debt spiral? The most obvious place to look is the spending side as taxes have not changed a whole bunch in my lifetime. They lower rates, but remove deductions. Then they raise rates, but add back in a bunch of deductions. As Reason Magazine noted a few years ago, tax collection remains fairly constant over time.

Here’s one of my favorite charts. It is the per capita inflation adjusted spending. Using 1980 as the starting point, the size of the Federal government has doubled, even adjusting for inflation.

When you look at per capita, inflation adjusted GDP growth, you see something curious. The average growth rate has been 1.86% since 1980, which is interesting for a number of reasons, but what’s relevant here is that it explains the chart above. The cost, per capita, of government may have doubled in 35 years, but so has per capita, inflation adjusted GDP. The cost of the Federal government has simply kept pace with rise of incomes. The relative cost of government has not changed much.

So, what is driving the debt spiral?

The answer is the the debt spiral is self-perpetuating in a zero interest rate world. Imagine you have a personal income of $100,000 per year after taxes and expenses of $105,000 per year. You borrow $5,000 to cover the deficit. Every year your earnings go up 5%, but your expenses go up 5% as well. In 20 years, that annual deficit is $12,500, which sounds pretty good. Your annual deficit percentage has not changed, but your total debt is now $165,000!

Of course, it gets much worse because debt has interest. Even the government pays something in interest today. Using the above example and the historic norm of 7%, the total debt would balloon to over $200,000 in that 20 years and the debt payments would eat up a big chunk of the budget. Long before you got the 100% debt range, your little country would have been forced to cut back and pay down debt.

What’s happened in the free money era since the 1980’s is the cost of borrowing, in the view of politicians, has disappeared. In the age of market based borrowing rates, the bond markets forced the government to choose between competing options. Do you spend more on defense or more on roads? Do you make pension promises for ten years out or does the impact on borrowing make that untenable, because it cuts into current spending on other constituents?

That has not been the case for a generation. Instead of choosing between competing interests, pols just borrow to pacify both interests. The Republicans borrow to cut taxes for their patrons and the Democrats borrow to give goodies to their patrons. Elections, therefore, have no consequences as the parties never threaten each others interest. The voters are simply deciding who gets to spend time at the debt trough.

Of course, there’s a limit to how much debt a government can run up even in a zero interest world. If central banks begin to let rates rise, then the day of reckoning comes much sooner, which is why they can never let rates rise, at least not on purpose. That returns me to the original topic. The only “tweak” that can fix the debt problem is actually a radical change and that comes but one way.

To keep Z Man's voice alive for future generations, we’ve archived his writings from the original site at thezman.com. We’ve edited out ancillary links, advertisements, and donation requests to focus on his written content.

Comments (Historical)

The comments below were originally posted to thezman.com.

11 Comments